Key Points

- Heavy insider selling across several high-profile tech names is raising questions about whether investors should treat the activity as a warning sign or routine profit-taking.

- Institutional buying and company-specific growth catalysts suggest the insider selling may not tell the full story for each stock.

- Valuation, analyst sentiment and upcoming earnings updates could determine whether these stocks keep climbing or face a sharper pullback.

Insiders are selling top tech plays and sending signals to investors. The question is whether investors should follow suit or if these are contrarian indicators in otherwise bullish markets. Insider selling is one thing if the company performs poorly or the outlook dims; it is something else entirely when the outlook is bullish, and stock prices are rising or expected to rise.

NuScale Power Corporation Insiders Sell in Q1 and Q2

NuScale Power’s (NYSE: SMR) insiders sold heavily in Q1 and Q2, raising red flags for investors. The caveat is that true insiders, those with C-suite positions in the business, ceased their sales in Q1, while the bulk of the activity came from early investors. Flour Corporation liquidated its position in a highly telegraphed move that weighed on market action while simultaneously removing an overhang. Now that Flour is out of the picture, the market is stabilizing, and the long-term outlook is improving. NuScale is well-positioned as a small modular reactor play in nuclear power and has solid sell-side support.

Institutional trends are robustly bullish. The group owns nearly 80% of the stock and, despite Flour’s liquidation of its stake, has, on balance, bought quarterly for over two years. The balance in early 2026 is approximately $4-to-$1, providing strong support with shares trading near long-term lows. Analysts' sentiment is bullish, but presents a headwind as of mid-2026. The consensus price target indicates substantial upside, approximately 50%, but sentiment and price target revisions have been bearish. As it stands, the stock carries a consensus rating of Hold, with low-end targets suggesting the floor is $7, a fresh low if reached.

This year’s catalysts include Federal assistance, including regulatory and administrative support. The Trump administration is pushing for space-based nuclear power generation by 2028, suggesting revenue could ramp up quickly in the coming years. Additionally, finalizing a power purchase agreement with the Tennessee Valley Authority will clear the pathway to recurring revenue and profitability.

Astera Labs Insider Selling Rises as ALAB Stock Soars

Astera Labs (NASDAQ: ALAB) insiders have been selling aggressively, with activity broad-based across executives and directors. The bearish signal is partly offset by the stock’s sharp rally: ALAB has more than tripled from its early April 2026 levels and is up roughly 300% over the past year, giving insiders a clear incentive to take profits. With insider ownership still around 10%, additional sales could continue.

Institutional activity reveals this group is buying the shares, accumulating ALAB's stock at an approximate $3-to-$1 pace in 2026. The reason is business demand, as Astera Lab’s connectivity products are critical to AI data center construction. They enable the high-speed, low-latency connections required for advanced AI applications. This year’s catalysts include new product launches and the inference boom.

Analysts' bullish trends also pose a hurdle for the market. ALAB’s price action outpaced sentiment at the consensus target and high-end range, setting the stage for a price correction. The question is when the correction may come and how deep it may get; the answer is that it may come at any time and could be deep. ALAB is nearly 40% above its consensus forecast and may need a robust catalyst to keep its price advancing. That may not come until later in the year.

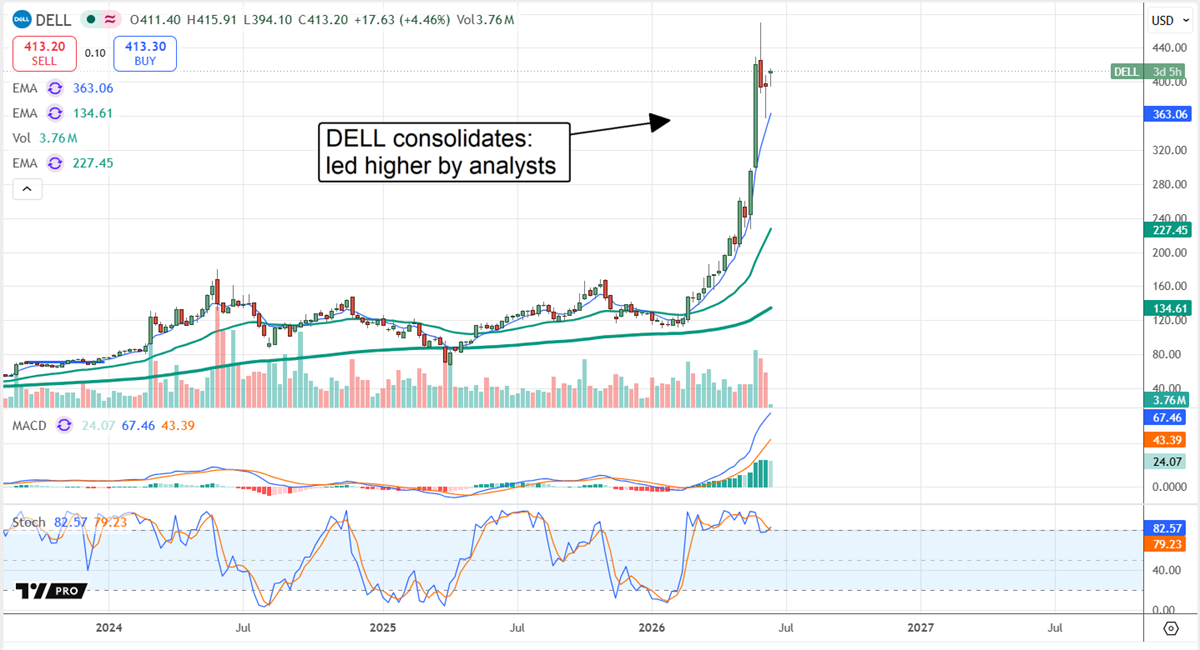

Dell Insiders Sell Into the Rally: Investors Can Do the Opposite

Dell (NYSE: DELL) insiders are selling into the rally, but a few caveats suggest investors should not do the opposite. The first is that Q2 selling is limited to Silver Lake Partners, an early investor and primary shareholder. It is selling shares to take advantage of the 2026 price spike, realize profits and return capital to its owners. Dell’s price is in rally mode, led by analysts who see it advancing to $700, or 70%, from mid-June levels. Dell, for its part, is delivering strong results, with its AI-optimized servers (built with NVIDIA GPUs) in high demand.

Institutions, aside from Silver Lake, are more bullish on this name. They collectively own over 70% of the stock and have accumulated it over numerous quarters leading up to Q2 2026. The risk is that the accumulation turned into distribution in Q2, which may limit upside as the year progresses. The visible catalyst is fiscal Q2 2027 results, expected in early September. Revenue is forecast to grow by more than 50%, and earnings by more than double that. However, NVIDIA's results are due out long before, providing the needed impetus. Its forecast is another quarter of sequential and YOY acceleration tied to AI GPU demand.

Companies in This Article:

| Company | Current Price | Price Change | Dividend Yield | P/E Ratio | Consensus Rating | Consensus Price Target |

|---|

| NuScale Power (SMR) | $10.59 | +7.1% | N/A | -3.63 | Hold | $15.92 |

| Dell Technologies (DELL) | $418.39 | +3.5% | 0.60% | 33.18 | Moderate Buy | $475.76 |

| Astera Labs (ALAB) | $387.57 | +7.1% | N/A | 261.81 | Moderate Buy | $233.75 |

Experience

Thomas Hughes has been a contributing author for InsiderTrades.com since 2019.

- Professional Background: Thomas Hughes is the Managing Partner of Passive Market Intelligence LLC, a market research platform he launched in 2023 with the mission: “We watch the market so you don't have to.” He has worked as a blogger, stock market commentator, and independent analyst since 2010 and has been actively involved in trading and investing since 2005.

- Credentials: He holds an Associate of Arts in Culinary Technology—training that honed his discipline, attention to detail, and ability to anticipate outcomes, all of which carry over into his work as a market analyst.

- Finance Experience: Thomas has been writing about finance and investing since 2011, when he discovered it could be more than a personal passion—it could be a profession. He’s been a contributing writer for InsiderTrades.com since 2019.

- Writing Focus: He specializes in the S&P 500, small-cap stocks, dividend and high-yield strategies, consumer staples, retail, technology, oil, and cryptocurrencies. His analysis blends chart-based technical setups with key fundamental insights, helping readers identify actionable trends.

- Investment Approach: Thomas takes a hybrid approach that combines technical analysis with deep fundamental research. He often writes about macroeconomic shifts, earnings trends, and sentiment-based trading signals.

- Inspiration: Thomas first became interested in stocks after attending a seminar on how to buy and sell your own shares. That event opened his eyes to the market's potential and sparked a lifelong interest in investing.

- Fun Fact: Thomas took up model railroading by accident a few years ago—and now he can’t stop running the rails.

- Areas of Expertise: Technical and fundamental analysis, S&P 500, retail and consumer sectors, dividends, market trends

Education

Associate of Arts in Culinary Technology